Show summary Hide summary

Oklahoma voters may soon be asked to decide whether to alter the state’s limits on property taxes — a change that could reshape local budgets, school funding and homeowners’ yearly bills. The proposal on the ballot would adjust how much property tax growth is capped, with immediate implications for homeowners, municipalities and public services.

What the measure would address

The ballot item targets the mechanism that restricts annual property tax increases. Currently, many states use caps to slow how quickly assessed values or tax bills can rise from year to year; the proposed change would modify that ceiling, changing either the method of calculation, the cap level, or both.

Oklahoma City Zoo celebrates surprise arrival of elephant calf

JCPenney Oklahoma: historic photos track the store’s evolution

Supporters say the adjustment is intended to ease the pressure of rising property assessments on ordinary homeowners. Opponents warn it could limit revenue for cities, counties and school districts at a time when local governments face growing costs.

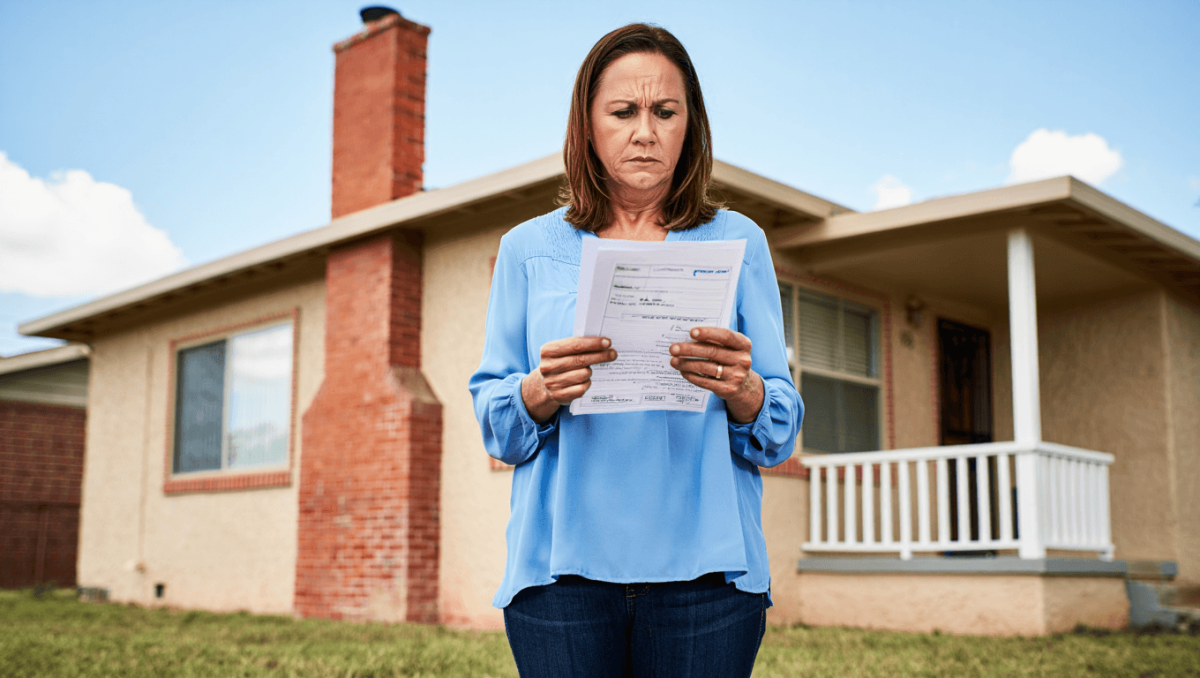

Practical consequences for residents

For individual homeowners the effect will depend on several variables: the size of the cap change, local assessment practices and whether officials shift tax rates to compensate. In places where property values are climbing rapidly, even a small change in the cap can alter the size of tax bills noticeably.

- Homeowners: Potential for slower annual increases in tax bills, but also greater variability depending on local rate adjustments.

- Renters: Indirectly affected if landlords pass higher or lower property costs through to tenants.

- Local governments: Could face reduced or more unpredictable revenue streams, complicating budgeting.

- Schools and public services: Funding for education, public safety and infrastructure may be constrained if caps lower available revenue.

How the finances could shift

Altering a tax cap rarely changes revenue uniformly across a state. Rural areas with stable values might see little immediate impact, while fast-growing urban and suburban communities could feel the effect sooner. That unevenness matters because many local governments rely heavily on property taxes for operating budgets.

| Sector | Possible short-term effect | Possible long-term effect |

|---|---|---|

| Homeowners | Smaller year-to-year increases in tax bills | Possible higher assessments later if rates rise to offset caps |

| Municipal budgets | Reduced or uncertain revenue streams | Pressure to cut services or seek alternative funding |

| Schools | Short-term squeeze on operating funds | Potential for classroom impacts unless state aid adjusts |

What to watch on the ballot and afterward

Voters should read the exact language of the proposal: small differences in wording — such as referencing “assessed value” versus “tax levy” or setting fixed percentages versus formulas tied to inflation — can produce very different outcomes. Pay attention to transitional rules and whether the change includes exemptions for seniors, veterans or low-income homeowners.

After a vote, implementation details matter most. Local officials may respond by changing millage rates, adjusting exemptions or pursuing new fees to cover shortfalls. State-level budget choices can also mitigate or amplify local impacts.

Ultimately, the decision on the ballot is less about a single number than about trade-offs: protecting taxpayers from sudden spikes in bills versus preserving predictable revenue for schools and basic services. Voters weighing the measure should consider how it interacts with local assessment practices and the broader fiscal picture in their community.