Show summary Hide summary

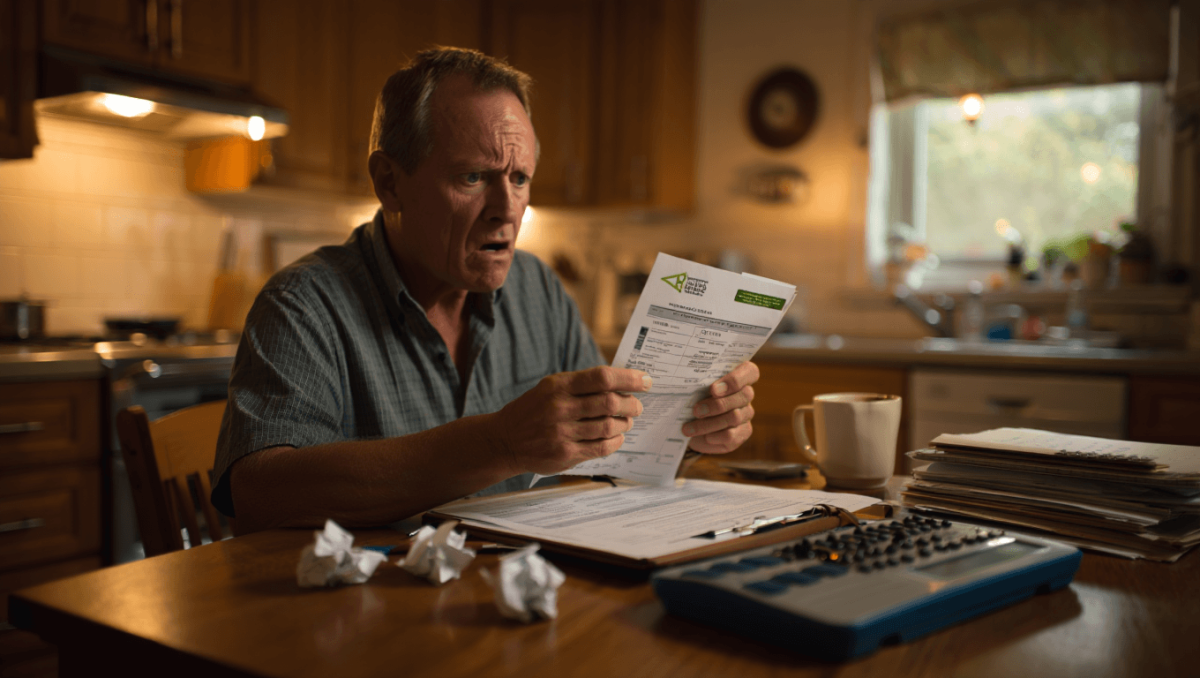

If your homeowners insurance bill has risen again this year, you’re part of a larger trend reshaping the housing market and household budgets across the country. Recent rate increases, insurer market moves and mounting repair costs mean homeowners face concrete choices now — from adjusting coverage to pressing state regulators for relief.

Why prices are climbing — and why it matters today

Insurers point to a cluster of immediate pressures: more frequent severe weather claims, rising construction and labor costs, and higher reinsurance premiums. Those forces have pushed many companies to file for premium hikes this year, and some are scaling back offerings in the riskiest areas.

OKConnect unveils platform to help business leaders strengthen community bonds

Azerbaijan jails nine journalists and activists: rights groups warn of new press crackdown

The result is not just a slightly larger monthly bill. Higher home insurance premiums affect mortgage approval costs, property values in vulnerable neighborhoods and owners’ ability to keep adequate coverage after a loss.

What’s driving the increases

Several factors are converging to lift homeowners insurance costs:

- Weather-related losses: Bigger, more frequent storms and wildfires generate larger claim volumes and payouts.

- Inflation in construction: Material and labor costs to repair or rebuild homes have risen faster than general inflation.

- Reinsurance and capital: Global reinsurers have tightened capacity or demanded higher prices, which insurers pass on to consumers.

- Underwriting changes: Insurers are re-evaluating which risks they will cover, tightening terms or excluding certain perils.

Insurance markets vary by state and even by county. In areas hit repeatedly by disasters, some carriers have increased rates sharply or withdrawn from the market entirely, leaving fewer options for residents.

Immediate choices for homeowners

You don’t have to accept the first renewal notice. Practical steps can limit the impact of higher premiums and reduce future exposure.

- Compare multiple quotes each year — rates and coverage vary significantly between companies.

- Ask about discounts tied to updates such as new roofs, impact-resistant windows or smart-home leak detectors.

- Consider raising your deductible to lower premiums, but ensure you can cover that cost after a loss.

- Document your property — photos and receipts streamline claims and help prevent underpayment.

- Explore catastrophe funds or state-backed options if private coverage is scarce in your area.

Policy traps to watch

As insurers tighten underwriting, some common pitfalls are appearing in policy language. Watch for narrowing definitions of covered perils, depreciation clauses, and coverage caps on rebuilding costs.

Replacement cost versus actual cash value is a critical distinction: the former covers the full cost to rebuild, the latter factors in depreciation and can leave owners underinsured.

What regulators and lawmakers are doing

State insurance departments have fielded a surge of rate filings and complaints. Some regulators are pushing insurers to demonstrate that proposed increases are justified, while others have approved hikes as actuarially necessary.

At the legislative level, lawmakers in several states are debating measures to stabilize markets — including public reinsurance programs, stricter oversight of rate-setting, and incentives for resilience upgrades that reduce claims over time.

Longer-term perspective

Expect insurance markets to keep evolving as climate impacts, construction economics and capital markets shift. For homeowners, the most reliable strategy is to focus on risk reduction and clarity:

- Invest in resiliency where feasible (e.g., fire-resistant landscaping, flood-proofing).

- Maintain clear records of improvements and valuations.

- Review your policy annually and ask your agent to explain any changes in coverage or exclusions.

Higher premiums can feel like an unavoidable burden today, but better-informed choices and a targeted mix of mitigation and shopping can limit the financial shock of future claims. For households in high-risk areas, the larger conversation about community resilience and market solutions will shape whether coverage remains available and affordable in the years ahead.